Executive summary

The automotive industry is in the grip of a paradox. OEMs are spending billions to develop vehicles that can sense their environment, reason about risk, and act without human intervention — yet the organisations building those vehicles still rely on annual planning cycles, manual decision chains, and systems that were not designed to communicate with each other. Vehicles are becoming autonomous faster than the enterprises that produce them.

This mismatch is no longer a strategic curiosity. In an industry facing simultaneous pressure from electrification, software-defined vehicle architectures, compressed margins, and intensifying competition from Chinese manufacturers who are outpacing Western OEMs on both cost and AI integration, decision latency has become a structural liability.

The answer is not more analytics or faster dashboards. It is Agentic AI: a new class of goal-driven systems that can sense signals across the enterprise, reason across constraints and objectives, and execute actions automatically within defined guardrails. Where predictive AI tells you what might happen and copilot tools help humans decide faster, agentic AI closes the loop — it decides and acts.

OEMs that build this capability into their operations over the next 24 months will establish a durable structural advantage. Those that treat it as a future consideration risk falling irreversibly behind — not on the road, but inside the enterprise.

The autonomy paradox

Ask any senior executive at a major OEM about autonomous vehicles and they will describe a sophisticated, well-funded programme. The investments are real: advanced sensor fusion, AI-powered driving stacks, over-the-air update architectures, and end-to-end software platforms designed to evolve long after a vehicle leaves the factory. Companies such as Volkswagen Group, Mercedes-Benz, Toyota, and Stellantis are collectively spending tens of billions of dollars to make vehicles that can see, think, and act.

Now ask the same executive how their organisation makes a pricing decision in response to a sudden market shift. Or how quickly their supply chain responds when a tier-two supplier signals a disruption. Or how long it takes to translate a demand forecast into a revised production schedule across multiple plants. The answers reveal a different reality: weeks, not hours. Committees, not systems. Reports reviewed after the fact, not actions taken in the moment.

This is the Autonomy Paradox: the technology a company builds for the road is decades ahead of the technology it uses to run itself.

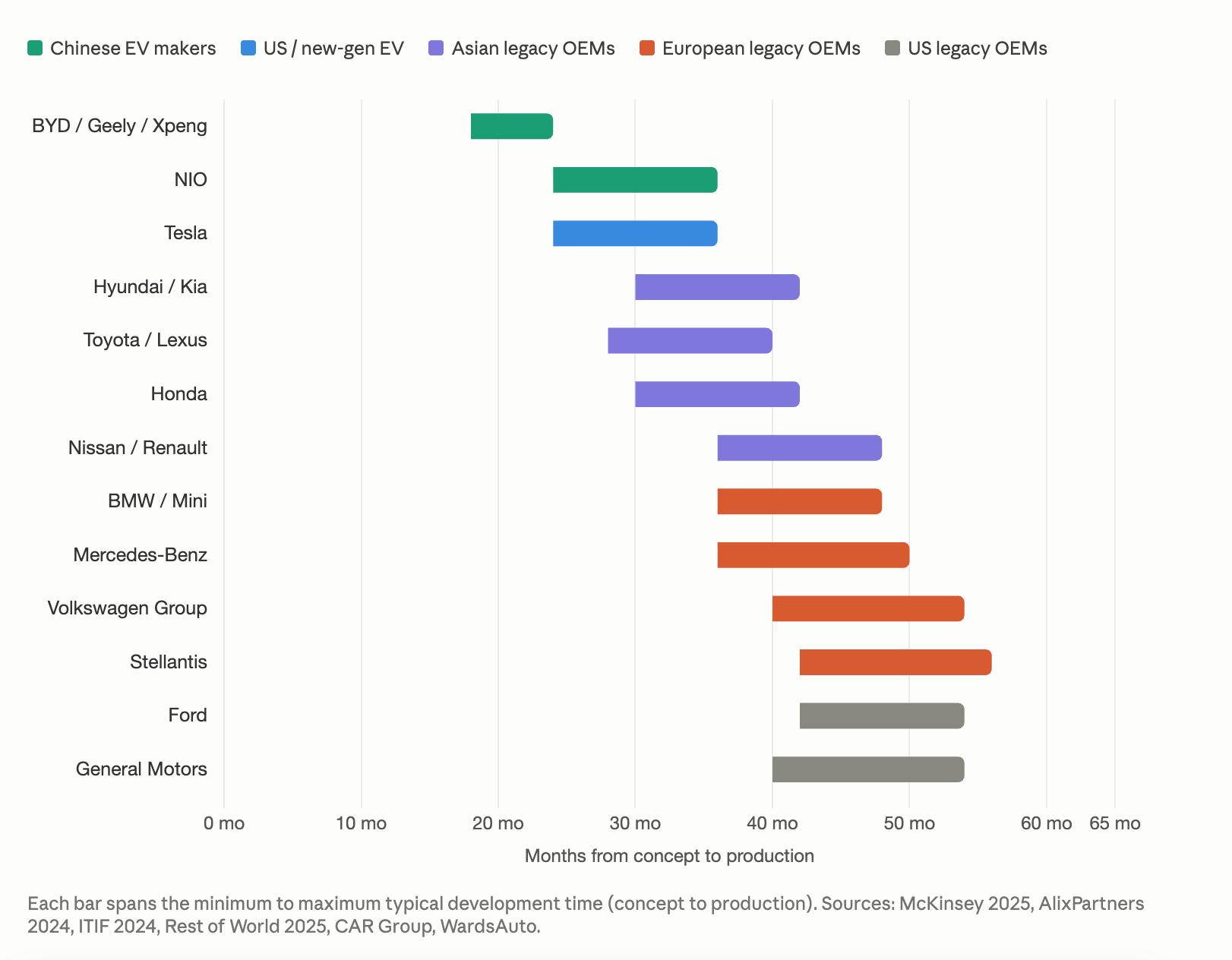

The consequences are becoming material. Margins across the industry are under severe pressure — legacy OEMs are fighting to protect profitability while managing the capital intensity of the EV transition and the cost of building out software capabilities. Meanwhile, Chinese manufacturers are demonstrating what a structurally lower-cost, higher-velocity operating model looks like in practice. They produce approximately 30 million vehicles annually — roughly twice North America’s output — and manufacture at 25–30% lower cost than anywhere else in the world. A significant part of that advantage is operational: AI is embedded not as a project but as a way of running the business.

There can be a point around how, because of this lag. Manufacturers spend 100 and thousands of dollars adding features on cars that customers will never use. And then spend millions in operational costs to maintain features, especially the connected car ones, that are used by a handful of people. And sometimes the customer demand has moved, what customers tell you what they want is different from what they actually use a year from now.

The competitive pressure is also visible in consumer behaviour. Research shows that 84% of Chinese drivers say AI features would motivate them to purchase a vehicle, compared to just 48% of European drivers. The gap reflects a different relationship with technology — and it is closing fast as AI-first Chinese EVs enter Western markets with price points and feature sets that traditional OEMs cannot match through incremental improvement alone.

The implication is clear: improving the vehicle is necessary, but not sufficient. The competitive battleground is widening. And the organisations that win will be those that learn to operate at machine speed — not just design and manufacture at it.

What is a self-driving enterprise?

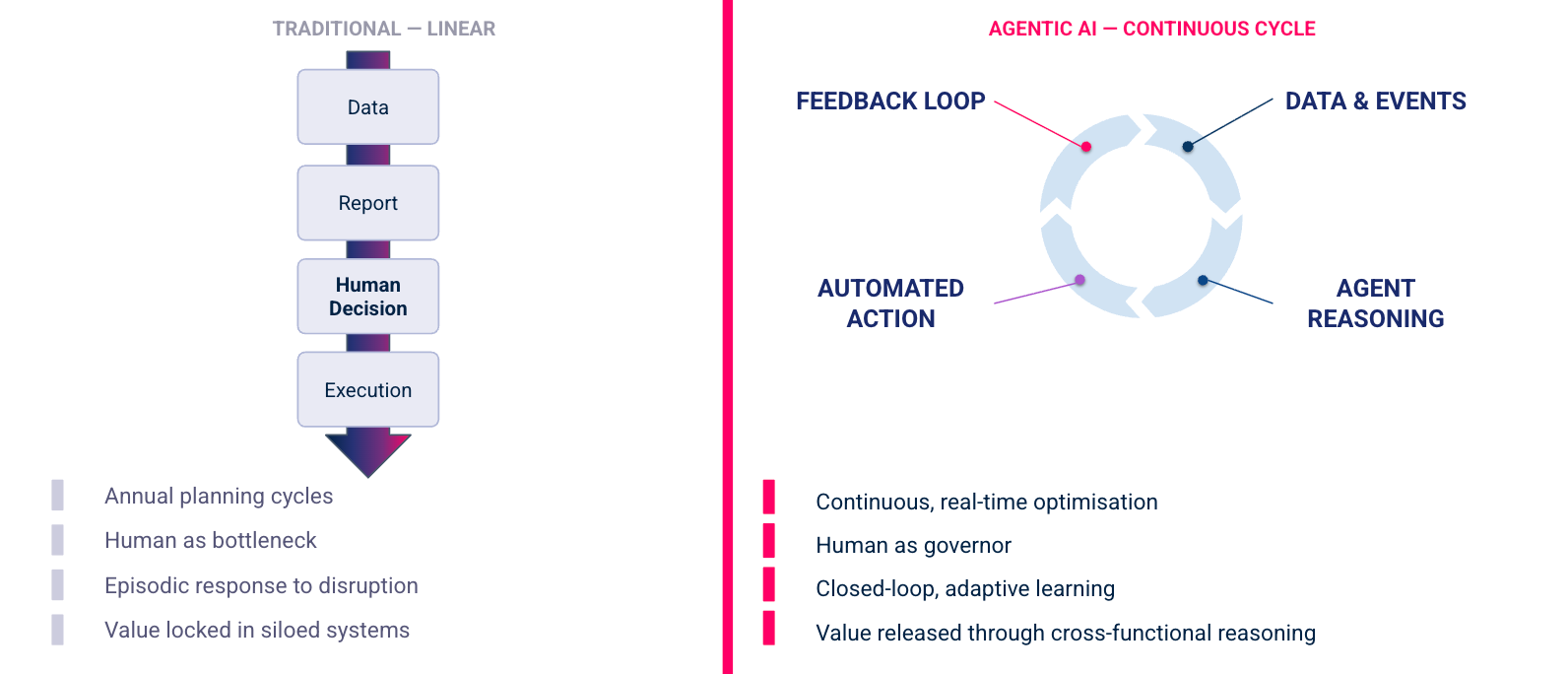

A Self-Driving Enterprise is one where systems continuously sense internal and external signals, reason across objectives and constraints, and execute actions automatically — with human oversight and governance, not human bottlenecks.

The distinction matters. This is not a vision of full automation or the removal of human judgment. It is a fundamental shift in where human attention is applied: away from operational coordination and toward strategic governance, exception handling, and continuous improvement of the systems themselves.

Consider a concrete illustration. Today, when a key supplier signals a potential shortage, an OEM’s response typically involves a series of escalations: a buyer flags the issue, a cross-functional team convenes, options are modelled manually, a decision is approved through layers of management, and instructions are issued to procurement and production teams. The elapsed time is measured in days or weeks. In a Self-Driving Enterprise, the same signal triggers an automated reasoning process: the agent assesses downstream impact across the affected production lines, evaluates alternative sourcing options against cost, lead time, and quality constraints, proposes or executes a replanning action, and logs its reasoning for human review. The response is measured in minutes, not days.

This is not robotic process automation, which automates narrow, rule-based tasks within a single system. It is not a copilot, which surfaces recommendations for a human to act on. And it is not a predictive model, which forecasts outcomes without closing the loop. It is something qualitatively different: a goal-driven system that reasons across multiple systems, weighs competing constraints, and takes action.

The shift is significant not just operationally but organisationally. In a Self-Driving Enterprise, data infrastructure, governance frameworks, and operating models are designed around the assumption that systems will act — and humans will govern and refine those actions. This requires a fundamentally different approach to process design, technology architecture, and workforce capability.

Agentic AI: The missing layer

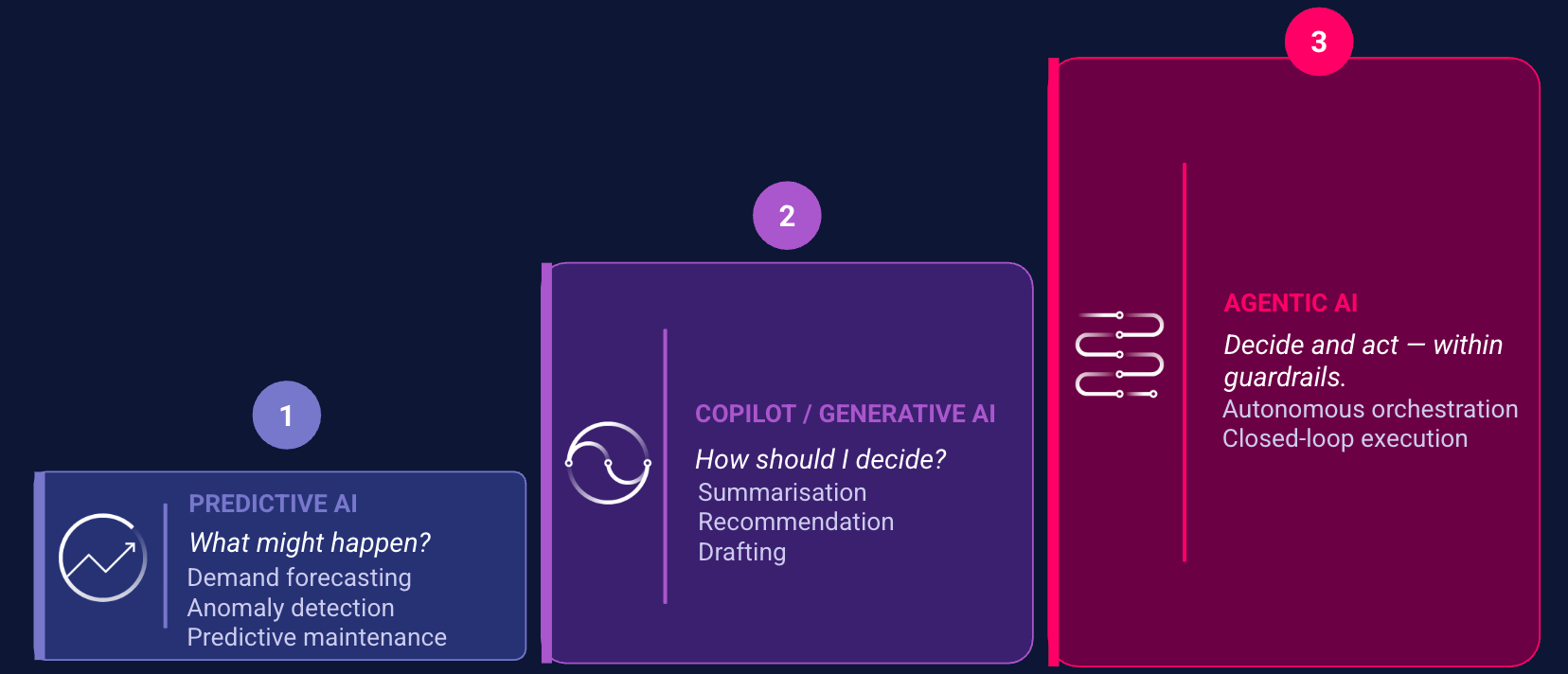

Most OEMs have made meaningful investments in data and AI over the past decade. They have built data lakes, deployed predictive models, and more recently begun experimenting with generative AI and copilot tools. Yet the gap between those investments and genuine operational autonomy remains wide. Understanding why requires being precise about what different classes of AI actually do.

Predictive AI — demand forecasting, quality defect detection, predictive maintenance — has delivered real value for OEMs. But it is fundamentally passive: it informs decisions without making them. A forecast of a supply disruption is only useful if someone acts on it quickly enough. Generative AI and copilot tools accelerate human decision-making, but they still place the human in the loop for every action. In a high-velocity, high-complexity operating environment, that remains a constraint.

Agentic AI is different in three important ways. First, it is goal-oriented: rather than responding to a specific query or generating a single output, an agent pursues an objective — minimising production downtime, maximising margin on a vehicle configuration, resolving a warranty cluster — by planning and executing a sequence of actions. Second, it is context-aware across systems: an agent can pull data from an ERP, a PLM, a supplier portal, and a market feed simultaneously, reasoning across them rather than working within any single tool. Third, it operates in a closed loop: it acts, observes the outcome, and adapts — continuously improving its own performance over time.

For OEMs specifically, this capability is uniquely powerful because of the nature of their operating environment. Automotive value chains are defined by massive interdependencies — a change in one node reverberates across dozens of others. A production schedule change affects supplier call-offs, logistics plans, dealer inventory, and cash flow simultaneously. A pricing adjustment interacts with demand, competitive positioning, residual values, and financial services products. These trade-offs are too complex, too continuous, and too time-sensitive to remain human-bound. Agentic AI is the missing layer that makes them tractable at machine speed.

The recent maturation of large language model reasoning capabilities, combined with the emergence of multi-agent orchestration frameworks, means that building production-grade agentic systems is no longer a research exercise. The technology is ready. The question for OEM leaders is whether their organisations are.

High-impact use cases across the value chain

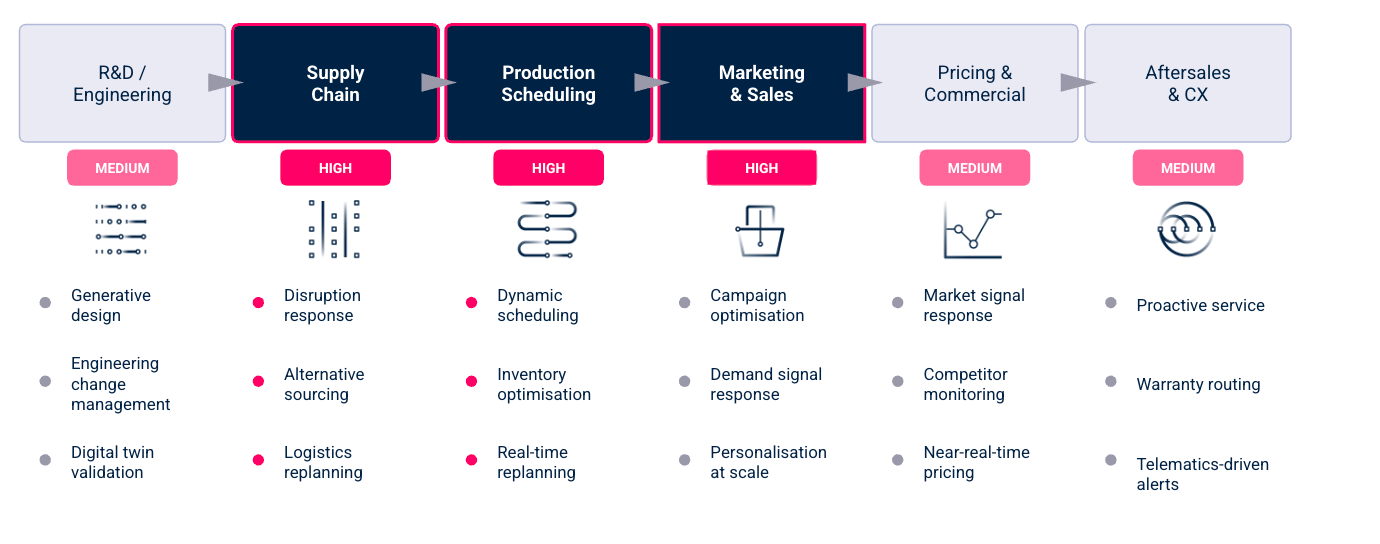

Agentic AI is not a solution in search of a problem. Across the OEM value chain, there are concrete, high-value processes where decision latency and human coordination overhead are creating measurable competitive and financial disadvantages. The following areas represent the highest near-term opportunity.

Design and engineering

AI is already beginning to transform how vehicles are conceived and validated. Generative design tools can explore thousands of engineering alternatives in the time a human team explores one. General Motors demonstrated this compellingly when they used AI to redesign a seat belt bracket: the system consolidated eight components into a single part that was 40% lighter and 20% stronger, evaluating over 150 design alternatives autonomously. Beyond individual components, digital twin and simulation capabilities are allowing engineers to run virtual validation cycles — including crash testing, thermal modelling, and systems integration checks — at a scale and speed that physical testing cannot match.

The agentic layer adds a further dimension: agents that monitor engineering change requests, assess their downstream impact across manufacturing and supply chain systems, flag conflicts, and route approvals automatically. In large OEMs where engineering change management can consume thousands of hours of coordination work annually, this represents a significant operational gain.

Supply chain orchestration

The supply chain is perhaps where the cost of decision latency is most immediately visible. The semiconductor shortage of 2021–23 demonstrated how quickly disruption at a single node could propagate across global production networks — and how the OEMs best positioned to respond were those with the most dynamic, data-driven operating models. Tesla’s ability to pivot during the chip shortage — rapidly rewriting firmware to accommodate alternative components and reconfiguring supplier relationships accordingly — was in part a function of AI-enabled supply chain visibility and responsiveness that legacy OEMs could not replicate.

Agentic supply chain systems continuously monitor signals across supplier networks, logistics providers, customs and regulatory environments, and internal production schedules. When a disruption is detected — or even anticipated — agents can evaluate alternative sourcing options, assess the cost and lead time implications of each, propose or execute a replanning action, and notify relevant stakeholders, all within minutes rather than days. The result is a supply chain that does not merely survive disruption but adapts to it in real time.

Production scheduling and plant operations

Production scheduling in a multi-plant OEM environment involves balancing hundreds of variables simultaneously: capacity across lines and shifts, sequencing constraints, inventory levels for thousands of parts, workforce availability, energy costs, and demand signals from markets that may change daily. Today, this is largely a human-intensive process, with planners spending significant time reconciling data from disconnected systems and making trade-off decisions that could be handled algorithmically.

Agentic scheduling systems can continuously optimise across these variables, dynamically adjusting plans in response to real-time inputs and learning from the outcomes of previous decisions. The gains compound: reduced idle time, lower inventory carrying costs, faster response to demand changes, and improved throughput — all without requiring human coordination at every step.

Pricing and commercial operations

Automotive pricing is one of the most complex optimisation problems in any industry. It involves balancing residual values, competitive positioning, dealer economics, financial services products, regional demand, and inventory levels — and it is changing faster than ever as EV adoption curves diverge across markets and Chinese competitors apply aggressive pricing strategies. Many OEMs still operate with pricing processes that run on weekly or monthly cycles, leaving significant margin on the table in rapidly shifting conditions.

Agentic pricing systems can monitor market signals, competitor moves, and inventory positions continuously, generating and executing pricing recommendations in near real time. When combined with agents managing dealer communications and financial services products, the result is a commercial operating model that responds to the market at market speed.

Marketing & customer experience

In the traditional OEM model, marketing is a linear process: brand strategy leads to creative briefs, which lead to agency execution, and finally, to media buying. This “relay race” is slow, expensive, and often disconnected from real-time market signals. The Self-Driving Enterprise reshapes the marketing function from a labor-intensive cost centre into a lean, high-velocity engine of growth.

In this reshaped function, the “Campaign Brief” evolves from a dead document into a dynamic, iterative dialogue; a lead marketer defines high-level business objectives, and an Agentic Orchestrator immediately interrogates the goal, scanning real-time inventory and competitor data to autonomously refine the strategy and channel mix.

This transition allows marketing teams to remain significantly leaner while increasing impact, as agents manage the “creative-to-delivery” pipeline—generating thousands of hyper-localised assets and navigating millions of 1:1 customer journeys simultaneously. By reasoning through individual friction points, such as why a prospect abandoned a configurator, agents deploy personalised interventions in real time, effectively harmonising global brand strategy with local dealer reality and individual customer intent.

Aftersales and customer operations

The aftersales value chain — warranty management, service scheduling, parts logistics, and customer communications — is both large in revenue terms and highly amenable to agentic approaches. Connected vehicles generate continuous telematics data that can signal maintenance needs, emerging faults, and usage patterns. Agents can process this data at fleet scale, triggering proactive service interventions, personalising customer communications, and routing warranty cases to the appropriate resolution pathway automatically.

Tesla has demonstrated the power of this approach: its fleet collectively generates driving data that improves everything from Autopilot to design decisions, creating a virtuous cycle of learning that is embedded into the product and the business simultaneously. Most legacy OEMs have millions of connected vehicles on the road but are not yet capturing or acting on this data at anything close to its potential. Agentic aftersales systems represent a direct path to closing that gap.

What is needed to make this happen

The technology for agentic AI is maturing rapidly. The greater challenge for most OEMs is not building the agents — it is creating the conditions in which agents can operate effectively. This requires enablers at two levels: organisational and technical.

Organisational enablers

The most common failure mode in enterprise AI is not technical: it is deploying sophisticated systems on top of broken or poorly designed processes. Agentic AI amplifies what already exists. If the underlying process is flawed, an agent will execute that flaw at speed and scale. Process reinvention — not just automation — must therefore precede or accompany agent deployment.

Governance is equally critical. Agentic systems that act without clear accountability structures, audit trails, and escalation mechanisms create operational and reputational risk. OEMs need to establish AI governance frameworks that define what agents are authorised to do, how their decisions are logged and explained, and how exceptions are escalated to human oversight. This is not bureaucracy — it is the foundation that makes autonomous operation trustworthy enough to scale.

Perhaps most importantly, the workforce must evolve. The shift to a Self-Driving Enterprise does not eliminate the need for human expertise — it changes the nature of that expertise. Planners, analysts, and operations managers will need to develop the skills to define agent objectives, interpret agent outputs, identify when intervention is needed, and continuously improve the systems they oversee. This requires investment in capability building and a genuine shift in how roles and incentives are structured.

Technical enablers

Three technical foundations are non-negotiable for effective agentic AI deployment in an OEM context.

- Real-time and event-driven data architectures — Agents need to sense and respond to signals as they happen, not as they appear in a batch report. This requires moving from periodic data refreshes to streaming architectures that surface events — a supplier shipment delayed, a quality threshold breached, a demand signal shifted — in real time.

- Shared semantic models — Agents reasoning across functions need a common language for the objects they operate on: products, plants, parts, customers, orders. Without shared definitions, an agent that spans procurement and production cannot reliably connect a purchase order to a production plan. Building and maintaining these shared models is unglamorous but essential.

- Trust layers: lineage, explainability, and auditability — For agents to be trusted with consequential decisions, every action must be traceable. What data did the agent use? What reasoning did it apply? What alternatives did it consider? These questions must be answerable — both for internal governance and increasingly for regulatory compliance.

Roadmap: The next 24 months

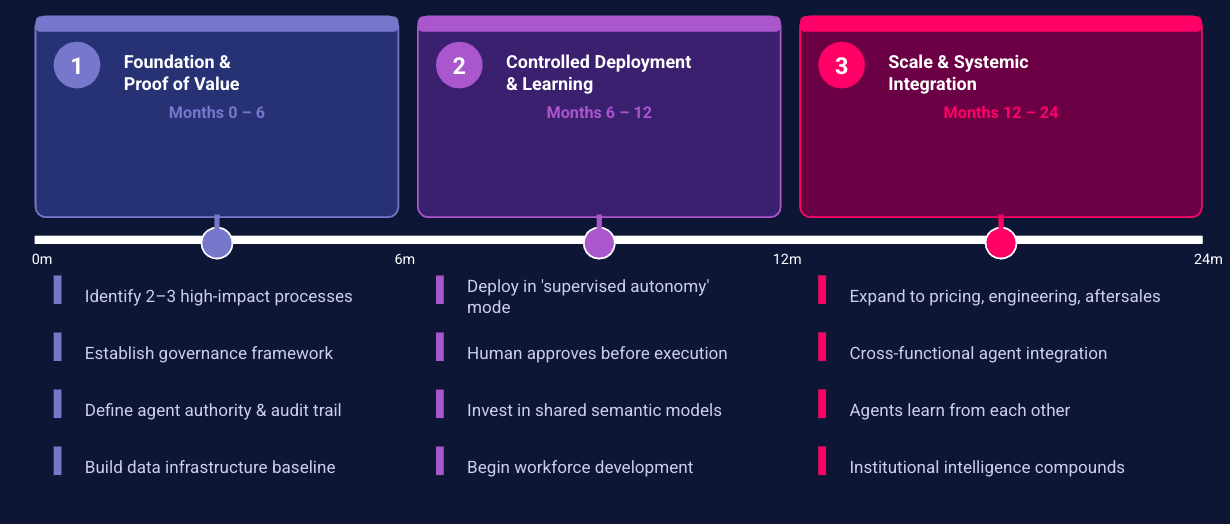

Becoming a Self-Driving Enterprise is not a single transformation programme — it is a capability that is built iteratively, starting with high-value, well-scoped interventions and scaling as confidence and infrastructure mature. The following roadmap reflects a pragmatic approach, calibrated to the organisational realities of a large OEM.

Months 0–6: Foundation and proof of value

The first priority is identifying two to three processes where decision latency is creating measurable cost or competitive harm — and where the data and integration foundations are close enough to production quality to support agentic deployment. Supply chain disruption response and production scheduling are strong candidates for most OEMs, given the volume of decisions involved and the directness of the financial impact.

Alongside process selection, this phase should establish the governance framework that will underpin all subsequent deployments: decision authority levels, audit and explainability requirements, escalation protocols, and the metrics by which agent performance will be evaluated. Getting governance right early is significantly easier than retrofitting it later.

Months 6–12: Controlled deployment and learning

Initial agents should be deployed in a ‘supervised autonomy’ mode: the agent reasons and proposes actions, but a human approves before execution. This builds organisational confidence, surfaces edge cases and failure modes, and generates the performance data needed to justify expanding agent authority. The feedback loop between agent outputs and human review is itself a valuable source of training signal.

During this phase, investment should continue in the technical foundations — particularly the shared semantic models and real-time data infrastructure that will be needed as agents expand across more processes and functions. It is also the right time to begin the workforce development programmes that will equip teams to govern and improve the systems they work alongside.

Months 12–24: Scale and systemic integration

As performance data accumulates and governance frameworks prove their effectiveness, the scope of agentic deployment can expand — both across more processes within proven domains and into new areas such as pricing optimisation, engineering change management, and aftersales operations. The most significant value creation in this phase comes from integration: agents that operate across functional boundaries and learn from each other’s actions, creating the closed-loop intelligence that defines a genuinely Self-Driving Enterprise.

By the end of 24 months, leading OEMs should have agentic systems operating across multiple value chain domains, a mature governance and auditability framework, and an organisational capability — in data engineering, AI operations, and change management — that compounds in value with each subsequent deployment.

Conclusion

Fully autonomous vehicles will take longer than expected to scale globally. Regulatory harmonisation, liability frameworks, safety validation, and infrastructure constraints remain unresolved across most major markets. The industry’s most optimistic projections for Level 4 and Level 5 deployment at scale have consistently been revised outward.

Autonomous enterprises can be built now. The technology is ready, the use cases are proven in adjacent industries, and the competitive pressure to act is intensifying. OEMs that deploy agentic AI across their operations will move faster, operate at lower cost, and learn continuously — building institutional intelligence that compounds over time. Those who wait will find the gap harder to close with each passing quarter.

The organisations that will define the next chapter of the automotive industry are not necessarily the ones with the most advanced vehicles. They are the ones who master the full equation: building machines that think on the road, while building enterprises that think inside the organisation.

The race to autonomy is not only on the road. It is inside the enterprise. And it has already begun.